The Prospectus Regime

At a European Level

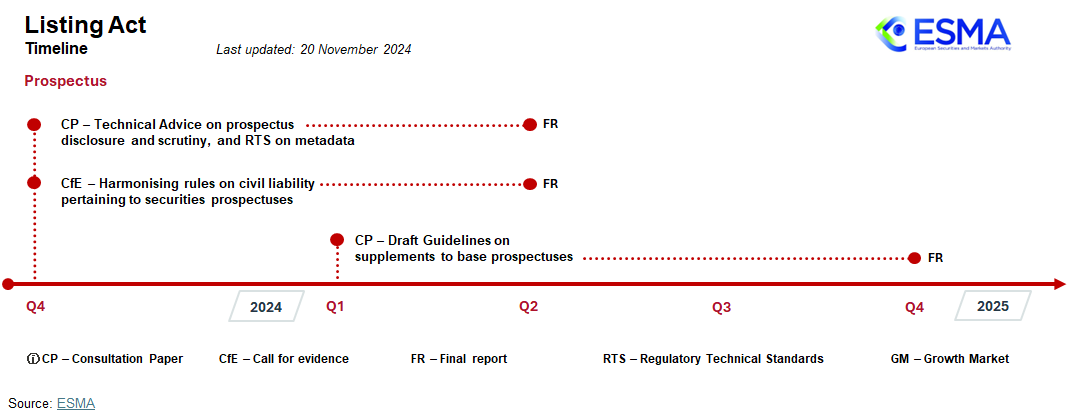

On 14 November 2024, an amending Regulation was published in the Official Journal of the European Union as part of the EU’s Listing Act Package (Listing Act)1. The amending Regulation makes important changes to the EU Prospectus Regulation2, with key provisions being implemented in 2024, and progressively between 2025 and 2026.

1The Listing Act Package is comprised of:

- An amending Directive amending Directive 2014/65/EU (MiFID II) and repealing Directive 2001/34/EC (Listing Directive),

- An amending Regulation amending Regulation (EU) 2017/1129 (EU Prospectus Regulation), Regulation (EU) 596/2014 (Market Abuse Regulation), and Regulation (EU) 600/2014 (MiFIR).

- A new Directive on multiple-vote share structures in companies that seek the admission to trading of their shares on an SME growth market.

2The focus of this page is on the Prospectus Regime, therefore, other significant amendments brought forward by the Listing Act are not addressed here.

Overview of the main changes

-

a. Incorporation by reference: Issuers of base prospectuses can incorporate financial information (annual or interim) published after the prospectus date. Supplements are only required if new financial information reveals significant or material changes.

- b. Historical financial information: For equity offerings, it will be sufficient to include in the prospectus financial information for the last two financial years (previously three), and for non-equity offerings, the financial information for the last financial year only (previously two).

- c. Risk factors: Issuers must clearly specify risks and assess their materiality, avoiding generic or disclaimer-style risk factors.

4. Exemptions. The exemption threshold for the offering prospectus requirement is raised from EUR 8 million to EUR 12 million, with Member States being able to lower this threshold to EUR 5 million. The exemption threshold for the offer of securities/admission of securities to trading, fungible with securities already admitted to trading on the same market is raised from 20% to 30%.

5. Other amendments

-

a. Scrutiny and approval. Streamlined and improved convergence of the scrutiny and approval of the prospectus by National Competent Authorities (NCAs).

- b. URD Regime. After an issuer has had a universal registration document (URD) approved by the NCA for one financial year, the subsequent URD may be filed without prior approval (reduced from two financial years).

- c. Grandfathering. Prospectus approved before 5 June 2026 will continue to be governed until the end of its validity by the version of the EU Prospectus Regulation in force on the day of its approval.

Level 1

- Regulation (EU) 2021/337 amending Regulation (EU) 2017/1129 as regards the EU Recovery prospectus and targeted adjustments for financial intermediaries and Directive 2004/109/EC as regards the use of the single electronic reporting format for annual financial reports, to support the recovery from COVID-19 Available here

- Regulation (EU) 2017/1129, of 14 June 2017, on the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market, and repealing Directive 2003/71/EC Available here

Level 2

-

Commission Delegated Regulation (EU) 2019/980, of 14 March 2019, supplementing Regulation (EU) 2017/1129 as regards the format, content, scrutiny and approval of the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market, and repealing Commission Regulation (EC) No 809/2004

-

Commission Delegated Regulation (EU) 2019/979, of 14 March 2019, supplementing Regulation (EU) 2017/1129 with regard to regulatory technical standards on key financial information in the summary of a prospectus, the publication and classification of prospectuses, advertisements for securities, supplements to a prospectus, and the notification portal, and repealing Commission Delegated Regulation (EU) 382/2014 and Commission Delegated Regulation (EU) 2016/301

-

Commission Delegated Regulation (EU) 2020/1272, of 4 June 2020, amending and correcting Delegated Regulation (EU) 2019/979 supplementing Regulation (EU) 2017/1129 of the European Parliament and of the Council with regard to regulatory technical standards on key financial information in the summary of a prospectus, the publication and classification of prospectuses, advertisements for securities, supplements to a prospectus, and the notification portal

-

Commission Delegated Regulation (EU) 2020/1273, of 4 June 2020, amending and correcting Delegated Regulation (EU) 2019/980 supplementing Regulation (EU) 2017/1129 of the European Parliament and of the Council as regards the format, content, scrutiny and approval of the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market

Level 3

-

ESMA Questions and Answers on the Prospectus Regulation - 3 February 2023

-

ESMA Public Statement - Update Prospectus - 30 September 2020

-

ESMA Public Statement - Applicability of Level 3 Guidance published under Prospectus Directive - 30 September 2020

-

ESMA Guidelines on disclosure requirements under the Prospectus Regulation - 4 March 2021

-

ESMA Guidelines on risk factors under the Prospectus Regulation - 1 October 2019

-

ESMA Guidelines on Alternative Performance Measures (APMs) - 5 October 2015 - and related Questions and Answers - 30 October 2017

Available here and here, respectively

-

ESMA update of the CESR recommendations - The consistent implementation of Commission Regulation (EC) No 809/2004 implementing the Prospectus Directive - 20 March 2013

Available here

Note3: According to ESMA, the ESMA Questions and Answers on Prospectuses and the ESMA update of the CESR recommendations apply to prospectuses drawn up under the EU Prospectus Regulation to the extent they are compatible with the EU Prospectus Regulation.

3ESMA’s Note available here

In Luxembourg

Law of 16 July 2019 on prospectus for securities and implementing Regulation (EU) 2017/1129, of 14 June 2017, as amended, on the prospectus to be published when securities are offered to the public or admitted to trading on a regulated market, and repealing Directive 2003/71/EC

CSSF Circulars and Q&A

- Circular CSSF 21/771 - Application of the guidelines of the European Securities and Markets Authority on disclosure requirements under the Prospectus Regulation Available here

- Circular CSSF 21/766 - Update of Circular CSSF 19/724 on technical specifications regarding the submission to the CSSF of documents under Regulation (EU) 2017/1129 and the Law of 16 July 2019 on prospectuses for securities and general overview of the regulatory framework on prospectuses Available here

- Circular CSSF 19/724 (as amended by Circular CSSF 21/776): Technical specifications regarding the submission to the CSSF of documents under Regulation (EU) 2017/1129 and the Law of 16 July 2019 on prospectuses for securities and general overview of the regulatory framework on prospectuses Available here

- CSSF e-Prospectus web application for the filing of prospectuses and related documents, as well as notification requests as of 1 March 2021 Available here

- CSSF New Final Terms submission form as of 30 November 2020 - 2 November 2020 Available here

- CSSF FAQ – The Prospectus Regime Available here

Last updated: 29 November 2024